Explore Incentives

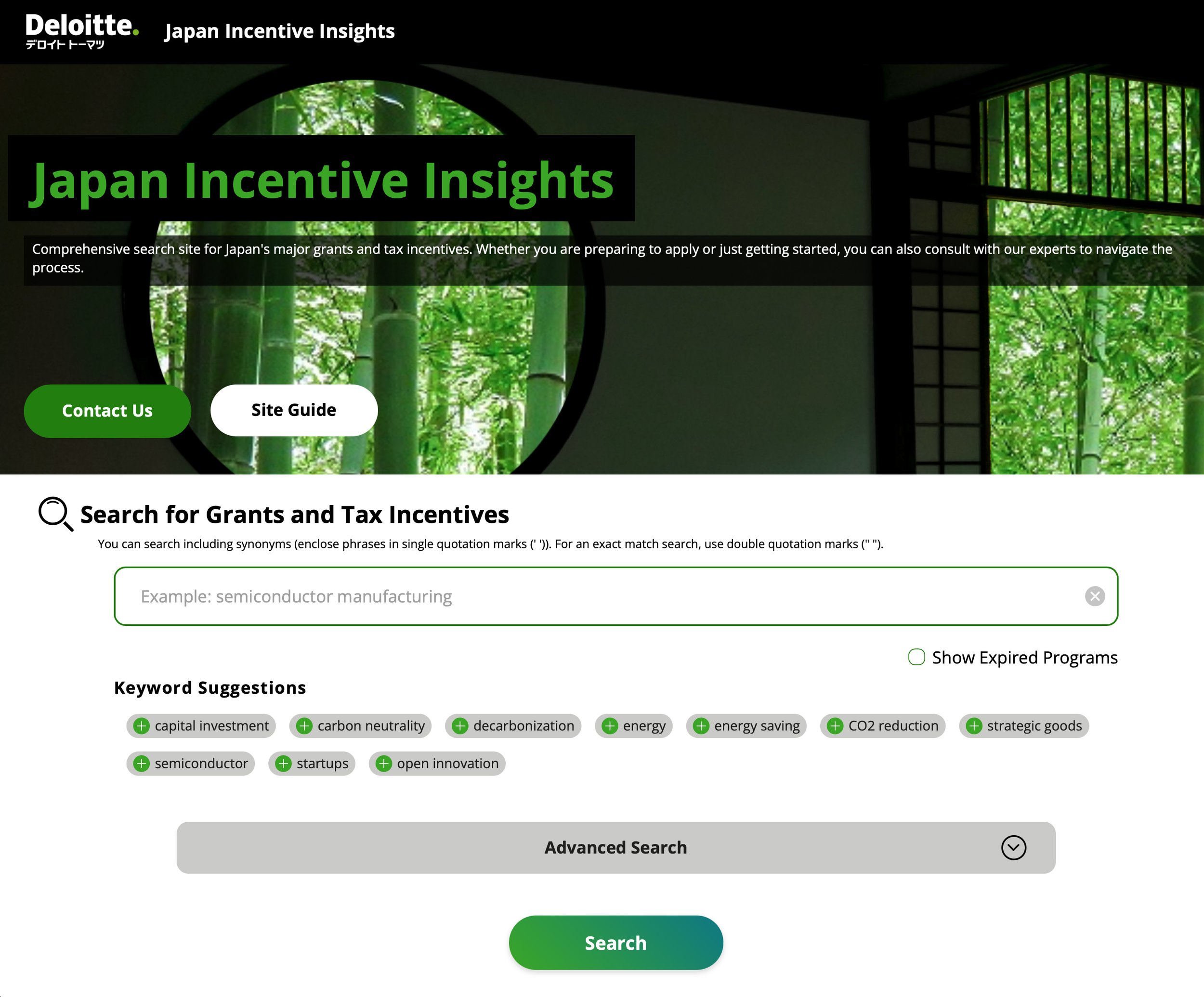

Deloitte Tohmatsu’s Japan Incentive Insights web tool helps companies find opportunities to invest in Japan.

Deloitte Tohmatsu’s Japan Incentive Insights web tool helps companies find opportunities to invest in Japan.

In Japan, where the population is declining, increasing foreign direct investment (FDI) is critical for sustaining economic growth. Despite an uptick in FDI, Japan’s inward FDI ratio to gross domestic product remains significantly lower than the OECD average, highlighting the urgent need to enhance locational competitiveness.

There are two main reasons why investment in Japan has not grown as expected: high business costs and high tax rates. To address these points and attract investment, both the Japanese government and local municipalities have established various support measures, including grants and tax incentives.

However, information about these incentives is often scattered across multiple websites and the availability of English-language information is limited. As a result, foreign companies considering investment in Japan frequently encounter challenges in gathering the necessary information and applying for these incentives.

To help foreign companies navigate these incentives and address the challenges of fragmented information and limited English-language resources, the Deloitte Tohmatsu Global Investment and Innovation Incentives team, Gi3, has launched Japan Incentive Insights, a website designed to promote the utilization of major incentives in Japan.

The Gi3 team comprises experts from Deloitte Tohmatsu Tax Co. and Deloitte Tohmatsu Immigration and License Co. and specializes in both domestic and international incentives.

By effectively utilizing grants, companies can mitigate high business costs and, by leveraging tax incentives, offset high tax rates. Additionally, in collaboration with other domestic tax teams and DT Legal Japan—which is part of the Deloitte Tohmatsu Group—Gi3 provides comprehensive consulting services related to tax and legal matters for foreign companies entering the Japanese market.

The Japan Incentive Insights website offers:

Incentive Search

Managed in accordance with the Certified Public Tax Accountant Act and the Certified Administrative Procedures Legal Specialist Act, Deloitte Tohmatsu Tax Co. handles tax incentives, while Deloitte Tohmatsu Immigration and License Co. oversees grants. The website aggregates information on more than 2,000 major incentives, searchable in English and Japanese, enabling foreign companies to easily gather the necessary information for investing in Japan.

Articles

Access a curated selection of feature articles highlighting noteworthy incentives and providing useful information for investing in Japan.

Consultation with Experts

Users can consult directly with Deloitte Tohmatsu through the website when proceeding with the application process for selected incentives.

Japan Incentive Insights supports both English and Japanese, making it an ideal tool for:

Headquarters of Foreign Companies

Search for incentives in English, switch to Japanese to obtain the exact Japanese names, and communicate efficiently with administrative offices or Japanese subsidiaries about the incentives.

Japanese Subsidiaries

Identify incentives in Japanese and provide the information to the overseas parent company without the need for translation.

Through Japan Incentive Insights, Deloitte Tohmatsu aims to strongly support foreign companies in leveraging Japanese incentives, thereby accelerating inbound investment and contributing to Japan’s economic growth.

Investor Nation

The ACCJ Financial Services Forum sets out a three-pronged strategy for stronger market policies in its latest white paper.

The ACCJ Financial Services Forum advocates for stronger market policies in its latest white paper

The American Chamber of Commerce (ACCJ) is fully on board with the Japanese government’s stated ambition of transforming the nation into a global leader in asset and wealth management, with the chamber’s Financial Services Forum (FSF) broadly supportive of a series of policy initiatives announced by Tokyo since April 2023. But they point out that more can be achieved to better meet consumers’ needs and that vigilance is required to ensure the promised changes do not stall.

The FSF comprises the leadership of the chamber’s five financial services committees and is designed to ensure that the ACCJ’s position on financial services issues is approved by the board and addressed in a consistent manner.

After a close examination of the government’s proposals, the FSF issued a white paper in July entitled Transforming Japan into a Global Asset and Wealth Management Leader. Stating that “the commitment that the national government is making to the transformation of the investment industry is critical for success, as most of the essential resourcing and policies can be achieved only with central government leadership, action, and education,” the paper details a three-pronged strategy:

- Accelerating corporate governance reform.

- Reforming the asset management sector and asset ownership.

- Doubling asset-based income among individual investors.

The FSF white paper outlines its recommendations within the context of the Government of Japan’s Policy Plan for Promoting Japan as a Leading Asset Management Center, released in December 2023. This framework serves as the foundation for the government’s efforts to transform Japan into a global asset management leader and financial hub.

Corporate Governance Reform

The first issue highlighted by the FSF is to accelerate progress on corporate governance reforms in parallel with reforms to the asset management industry. The goal is to make Japan a global standard bearer by sharply increasing participation among individual investors and expanding access to asset-based income.

There is clear common ground with many of the plans of the Japanese government, some of which is outlined in a June 2024 statement entitled “Principles into Practice,” issued by the Council of Experts Concerning the Follow-up of Japan’s Stewardship Code and Japan’s Corporate Governance Code. This council operates under the joint secretariat of the Financial Services Agency (FSA) and the Tokyo Stock Exchange (TSE).

The Japanese proposals emphasize greater corporate governance enforcement, training for independent directors, and stewardship activities, while the TSE has revised its listing rules to mandate English disclosures of financial statements and timely information effective April 1, 2025.

The FSF white paper makes clear, however, that many issues—including ensuring substantive reforms take root and enforcing deadlines for strategic shareholdings—remain incomplete or are still works in progress. Similarly, disclosure practices have improved, it points out, but there are concerns that some companies are still “going through the motions” instead of devoting the required effort to the procedures. Equally, there has been progress on efforts to unwind cross-shareholdings, although the paper emphasizes that greater reviews are still necessary.

“Stating that ‘the commitment that the national government is making to the transformation of the investment industry is critical for success, as most of the essential resourcing and policies can be achieved only with central government leadership, action, and education,’ the paper details a three-pronged strategy.”

“Board independence and diversity, progress on English-language disclosure, and electronic voting rights are cited as key improvements,” the white paper states. Transforming corporate governance “from a box-ticking exercise to a core business element” has received the strong support of Hiromi Yamaji, president of the Japan Exchange Group. This is seen as very important, but the white paper points out that “greater and quicker progress is needed to avoid complacency setting in among management, which could cause reform to stagnate.”

To ensure that does not happen, the FSF is calling on the FSA and the TSE to collaborate on a plan for stronger enforcement of the Corporate Governance Code and that the present recommendation that independent directors account for a minimum of one-third of Prime Market boards be increased to an outright majority. They would also like to see a new initiative to increase both the number and quality of training programs, with a focus on diverse director candidates.

Other proposals include making the recently extended tax incentives for spin-off companies permanent to enhance predictability when it comes to tax planning, promote the creation of innovative spin-offs, and optimize business portfolio strategy and planning. Yet another proposal in the white paper is for the TSE to work with listed companies to spread annual general meetings across the calendar and to permit virtual attendance by offshore investors.

Asset Management

Turning to asset management, 2023 legislation imposes a legal obligation on all parties in the investment chain to act in the best interest of customers. As the government implements its plan to translate this obligation into rules and regulations and/or codes of conduct for each set of players and actively enforce them, the FSF recommends that the FSA continue to take steps to strengthen measures that ensure the independence of asset management firms and improve the capabilities of management. It is also recommended that the FSA aggressively shift to a domestic retail brokerage revenue model from one dominated by transaction fees so that advisory fees become more important.

Other proposals include the introduction of a “comply-or-explain” approach to new standards, as well as formalizing a continuous process of monitoring implementation, with the outcomes published regularly and transparently.

Organizations beyond the ACCJ have also welcomed efforts by Japan to implement reforms in the asset management sector. The Washington DC-based Investment Company Institute (ICI) said in a July 1 statement:

“The Japanese government’s policy plan for the coming year consists of extremely important reforms, such as changes to Japan’s individual defined contribution retirement program, including increasing contribution limits and providing more opportunities for older workers to save,” said ICI President and Chief Executive Officer Eric J. Pan. “These reforms can help households adapt to changing macroeconomic conditions by making greater use of the diversified investments offered by asset managers to build household wealth, prepare for retirement and meet other important financial objectives.”

NISA and Asset-based Income

Pan also applauded the expansion of the Nippon Individual Savings Account (NISA) program through the simplification of operational procedures and promoting more people to take advantage of the scheme.

The changes to NISA were outlined by then-Prime Minister Fumio Kishida in a speech to the Economic Club of New York in September 2022 as a way of attracting more overseas companies into Japan and improving the offerings of the asset management industry. In a similar speech in September 2023, Kishida announced plans to establish special business zones for asset management firms where administrative procedures can be completed entirely in English. The administation of Prime Minister Shigeru Ishiba has committed to continuing this important initiative.

This initiative ties in neatly with the third focus of the FSF’s white paper, individual investors and asset-based income, with the report pointing out that in comparison with the US and European markets, “Japan’s individual investment and retirement market has enormous growth potential and opportunities to better serve the needs of investors, which is particularly important in view of Japan’s demographic and fiscal challenges.”

The FSF recommends further expansion of NISA limits as well as the range of investments that would qualify. The fact that flows into NISA accounts have increased dramatically in response to the previous increase of annual investment limits to ¥3.6 million underlines just how popular this form of investment is becoming.

Stronger Market

Placing priority on developing and resourcing programs that nurture an ecosystem of independent financial advisers—and where individual investors can receive advice free of influence from the companies that are offering products—is another evolution called for in the white paper. This would strengthen the quality of financial advisers and enhance client–adviser relationships.

The FSF’s proposals may be ambitious and far-reaching, but the forum is confident that, if adopted, they can deliver benefits to both consumers and providers in the Japanese market, as well as transforming Japan into a global asset and wealth management leader.

Japan to Foster Global Cooperation at the G7

In May 2023, the G7 Summit will be hosted in Hiroshima against the backdrop of a severe global energy crisis and supply chain disruptions that are stoking the fires of inflation, shaking consumer confidence, and threatening the most economically vulnerable in our society. METI will focus on three key policy areas: trade, climate and energy, and digitalization.

METI focuses on three key policy areas: trade, climate and energy, and digitalization

In May 2023, the G7 Summit will be hosted in Hiroshima against the backdrop of a severe global energy crisis and supply chain disruptions that are stoking the fires of inflation, shaking consumer confidence, and threatening the most economically vulnerable in our society.

Climate change, Covid-19, and Russia’s aggression against Ukraine are fueling global concern. In a speech given at the Center for Strategic and International Studies in January, Yasutoshi Nishimura, Japan’s Minister of Economy, Trade, and Industry, expressed his alarm, saying “the global shocks that have occurred, one after the other in the span of only a little more than two years, have truly been a wake-up call.”

All three challenges are likely to be high on the agenda at the G7 Summit and relevant ministerial-level meetings to be held throughout the year. The Ministry of Economy, Trade and Industry (METI) will take the lead at the ministerial meetings, along with relevant ministries, and aims to drive discussion and policy action in three key areas—trade, climate change and energy, and digitalization.

Revitalizing Global Trade and Investment

Trade is a key policy issue, especially given the rise of serious supply chain disruptions due to Russia’s devastating war in Ukraine.

“Russia’s aggression against Ukraine has shaken the international order, and there are concerns about a global economic slowdown,” said Takuya Kimura, principal director of METI’s Multilateral Trade System Department. “At the G7 meetings, we would like to emphasize the importance of upholding the free and fair economic order.”

Topics will include:

- Promotion of trade and investment

- World Trade Organization reform

- How the G7 will deal with unfair trade practices that distort markets

- Proposals for strengthening economic security

Even if these key issues are addressed, the global economy faces insurmountable hurdles without the existence of healthy trade and investment relationships between nations. METI’s work at the upcoming G7 Summit will include laying the foundation for future progress.

Around the world, shortsighted trade practices could lead to unfair trade. Such practices include forced technology transfer, whereby foreign companies operating in a host nation are required to carry out all processes—from design and development to the manufacturing of advanced technology products—in that nation, possibly forcing companies to share their sensitive technologies with the host nation’s companies.

Nishimura said that we must build a world where “countries will come together based on trust and strengthen their cooperation under the banner of free trade, without slipping into protectionism.”

Climate Change and Energy in Focus

Japan is looking to promote green transformation, or GX, which can rewrite the rules of the prevailing socioeconomic system by inducing transformational changes, without shoehorning emission reductions and economic growth into an either-or relationship.

“Green transformation is a major keyword in Japan,” explained Shinichi Kihara, deputy director general for technology and environment at METI. “The idea is that emissions reduction and economic growth are not in a trade-off relationship. Instead, they can coexist.”

GX will not stop at Japan’s borders, and the government will make efforts to approach countries responsible for major emission outputs while also providing appropriate support to developing nations that are in the process of transitioning to a green regime. Ultimately, Japan seeks to promote GX in all sectors, including energy and industry.

At the same time, the energy crisis has put the spotlight on global energy security. Nishimura believes it is necessary to undertake decarbonization in a way that is fully compatible with ensuring a stable supply of energy, and that it will be important to undertake various and practical pathways that fit the needs and expectations of individual nations.

Japan will make the utmost efforts to promote its clean energy transition, including installing the greatest possible amount of renewable energy facilities and using nuclear plants as much as possible.

Minister Yasutoshi Nishimura

Boosting Digitalization

Another major transformation underway is digital transformation, or DX, which has been defined as the creation of new value through innovation made possible by the adoption of digital technology that aims for the creation of a more prosperous society. The role of digitalization as a bulwark against unpredictable events has been highlighted in recent years by global challenges such as the Covid-19 pandemic and Russia’s aggression against Ukraine.

The free flow of data in the face of arbitrary restrictions and ensuring data integrity are essential if the digitalized world is to operate as intended.

In a move that has garnered positive international feedback, Japan proposed a guiding principle, Data Free Flow with Trust (DFFT), which seeks to enable cross-border free flow of data while addressing privacy, data protection, intellectual property rights, and security concerns. The principle was first suggested by then-Prime Minister Shinzo Abe at Davos 2019, and later endorsed at the G20 Osaka Summit in June 2019. Since then, the DFFT has been widely accepted as a primary principle for international digital policy coordination in various international forums.

Reaching a global consensus or convergence on the rules that involve privacy and security will take time. The G7, currently under Japanese presidency, is expected to formulate the priorities in operationalizing the DFFT so that countries can work together despite their varied approaches to data governance. Vigorously moving the DFFT into its operational phase, the Japanese government has announced that it will establish an institutional arrangement to promote interoperability across data regimes, implement the priorities that have been identified by the international forum, and advance solutions for cross-border data transfer through public–private cooperation.

It is also important to redesign governance for a digitalized society. DX technologies, such as artificial intelligence, the Internet of Things, and the metaverse, now have the ability to fundamentally reshape the way companies operate and how individuals relate to society.

It is vital to explore new governance options, including involving multiple stakeholders in discussions on how to flexibly update governance systems in response to changes in the operating environment.

International Cooperation Is the Only Way Forward

At the end of the day, the G7 is not just about the interests of advanced industrialized nations, but about building a way forward together with the entire international community.

“In 2023, Japan will host the G7 Summit, and the United States, India, and Indonesia will chair APEC, the G20 Summit and ASEAN, respectively,” Nishimura said. “While working in cooperation to deal with global-level issues, we will lay out for the international community a path forward for building a new economic order.” It will be also essential for Japan to work in coordination with the Global South to tackle various global challenges. “Japan, working within that partnership, is fully determined to fulfill its significant responsibilities.”

The Yen’s Fall from Grace

The Japanese yen is on track toward a parabolic move, with global and Japanese macro players set to become increasingly aggressive in betting on an overshoot toward ¥150–160 to the US dollar. Economist Jesper Koll examines the causes, the potential impact, and when the winds may shift again.

Who will stop it? When and why?

Listen to this story:

The Japanese yen is on track toward a parabolic move, with global and Japanese macro players set to become increasingly aggressive in betting on an overshoot toward ¥150–160 to the US dollar.

Why? Because the same economic forces that pulled the yen out of the remarkably stable range of ¥105–110 to the dollar, in which it was boxed for the past six years, are poised to get even stronger in the coming months. No mystery, no magic, no speculative excess. We got to ¥128–131 because of a decoupling of monetary policy. With Bank of Japan (BOJ) Governor Haruhiko Kuroda digging in his heels and the US Federal Reserve now floating the idea of accelerating the pace of rate hikes to possibly 75 basis points a pop, it very much looks like the yen’s slide is just beginning.

Policymakers: United America versus Disjointed Japan

The United States is mobilizing an all-out attack on inflation—raising rates and cutting the central bank balance sheet while, importantly, policymakers, politicians, and opinion leaders are busy signaling that more aggressive monetary tightening will have to come. Nobody knows how many rates hikes are necessary, or when the US monetary brakes will start to cut into demand, but everyone agrees that a strong dollar is good for the United States’ fight against inflation. After all, it reduces import prices.

Japan, in contrast, has a central bank that goes out of its way to keep on buying 10-year government bonds, determined to assure markets—through both action and talk—that nothing has changed, that deflation is still viewed as a bigger threat than inflation.

More importantly for investors looking for clues about the yen’s direction, neither the BOJ nor the Ministry of Economy, Trade and Industry, the Ministry of Finance (MOF), politicians, nor pundits agree on whether a weak yen is good or bad for Japan. Yes, everyone does agree that imported inflation is bad inflation, but many hope that a cost-push shock is just what is needed to break Japan’s deeply entrenched deflationary mindset and expectations. Remember: not so long ago, Nobel Prize winner and chief US economic commentator Paul Krugman, along with others, argued that an inflation target of seven to eight percent may be necessary to snap Japan out of deflation.

“Neither the BOJ nor the Ministry of Economy, Trade and Industry, the Ministry of Finance (MOF), politicians, nor pundits agree on whether a weak yen is good or bad for Japan.”

Personally, my work and investments away from macro theory, hands-on deep-dives into Japanese companies dealing with corporate chief executive officers and institutional chief information officers, and direct policymaking engagement with Japan’s industrial structure and demographic realities all have me convinced that inflation/deflation in Japan is not much of a monetary phenomenon, but primarily a regulatory and structural one.

Specifically, capital markets here are more or less explicitly designed to function far differently from the capital return-maximizing axioms underlying most of monetary policy theory in general, and the transition channels from central bank action to private capital allocation in particular. In my view, Japan Inc. works more in spite of monetary policy rather than because of it. Japan’s elite is far too pragmatic and realist than to entrust allocation of capital to some textbook theoretical models or economics dogma (particularly when they come from Chicago … just kidding).

But what may be true for the economy is not true for the currency. The yen is very much a slave to the masters at the BOJ and MOF. (Arguably, the yen is the only major capital market in Japan where, after decades of deregulation and liberalization, capital does flow relatively unencumbered. For example, it follows neoliberal market principals much more so than is the case in the bond, credit, or even equity markets. This has led to a relative loss of control, with both institutional and retail investors now much less influenced by “administrative guidance” than they were in previous decades.

An Asymmetric Risk

So, right now, if your job is to make money investing in currency markets, the contrast between a united US policy elite beginning to act—and poised to do so more aggressively (on the monetary front)—and a disjointed Japan elite only barely beginning to build consensus on a potentially necessary change, you’d be a bold trader to go against the rising US rates; and stable Japan rates equal weaker yen trade.

That’s why I think an overshoot toward ¥150–160 to the dollar is more probable than a return to the ¥105–110 range seen until a couple of quarters ago. Speculating against the yen has an asymmetric risk–reward profile now.

How long will this last? What forces could break the current dynamics? Yes, eventually Japan will follow the US lead. The BOJ always does. The one time it did not—and insisted on a decoupling from US policy—Japan got its bubble economy. Nobody, least of all Prime Minister Fumio Kishida, wants to go through that again.

Photo: gintsivuskansphoto/123RF.COM

Can Kishida Change Kuroda’s Mind?

Probably not. At least not until it becomes clear that Kishida is here to last. There is an upper house election in July. After that, yes. Kishida gets to appoint Kuroda’s successor early next year. If, by then, inflation becomes a political problem, Kishida may be well advised to pick an inflation hawk. That, however, is at least six to eight months away—an eternity for currency markets.

Again, the contrast between the United States and Japan is striking. For President Joe Biden, inflation is an immediate danger—a key reason for his continuing drop in popularity. Against this, Kishida’s popularity keeps climbing, and inflation running at barely one percent is far from becoming a political make-or-break issue. However, if, against the odds, the prime minister were to pick an open fight with the BOJ before the election, he is more likely to add to a yen-depreciation speculative frenzy.

Why?

First, Kuroda is both intellectually proud and politically pragmatic. He won’t risk his historic legacy of being the governor who beat deflation without seeing firm evidence of genuine demand-pull inflation. He does not want to go down in history as yet another BOJ governor who tightened too early. And, politically, he understands more than anyone the risk that rising interest rates pose to Japan’s fiscal flexibility. With public debt at nearly 2.5-times national income, public finances will be the biggest loser if and when interest rates go up too early (i.e., before domestic demand has entered a self-sustaining upcycle).

Second, markets want to see action and facts, not talk and debate. Show me the money. And with most forecasters now predicting an outright economic contraction during the latest quarter, it’ll get even harder to deny that Japan is indeed at the opposite end of the business cycle from the United States. Again, it is difficult to argue against the yen depreciation momentum accelerating in the immediate future.

When the Facts Change

But what about longer term? What structural dynamics might unfold that could trigger a reversal of fortune for the yen? Here are five primary moves that can or will force a change of direction from yen depreciation towards appreciation:

- The United States or China accuses Japan of starting a currency war

- The United States falls into recession

- Global investors, corporates, or tourists start buying Japan assets

- Japan’s investors and corporates start buying yen assets

- The BOJ starts following the Fed

From Fears of a Yen-led Currency War

Right now, the risk of Japan being accused of starting a currency war is low. If I am right and the US elite is indeed united in fighting inflation, it will continue to welcome a strong dollar and weak yen.

But what if China were to complain about excessive yen weakness? They did so the last time the yen weakened past ¥135–140 to the dollar in mid-1998. At that time, China successfully persuaded the Clinton administration to publicly abandon the strong-dollar policy that the United States was running at the time.

But times have changed. In 2022, Chinese complaints are unlikely to get much of a hearing in Washington. In 1998, the United States was focused on getting China to join the World Trade Organization and was happy to try and be helpful. Today, the United States regards China as its principal competitor, while Japan’s position as its principal ally in Asia is firmly reestablished. The more you believe the New Cold War rhetoric as an overarching US policy priority, the less you will worry about China triggering an end to yen depreciation.

US–China Agreement on Renminbi Devaluation?

However, rather than being lulled into a false sense of security by mainstream rhetoric, a pragmatist investor will constantly evaluate actual policy developments. Specifically, the latest overtures to China made by US Secretary of the Treasury Janet Yellen, suggesting US readiness to negotiate on reducing punitive tariffs still placed on US imports, is a potentially very significant about-turn in US–China economic policy.

Will US economic policy pragmatism prevail after all? Because, yes, Americans spend almost four times more on imports from China than they do on imports from Japan ($541 billion versus $140 billion in 2021). If a weak yen and strong dollar are good news for US consumers, a weak yuan is potentially four times more powerful.

No matter what the new cold warrior rhetoric says, given the deceleration of China growth and threats from asset deflation, the immediate economic policy (and domestic political) goals of China and the United States are now complementary—China wants inflation, the United States wants deflation.

Although very much a long-shot, given Biden’s industrial policy priorities—less from China, not more—a restart of US–China trade negotiations may set the stage for a devaluation of the yuan implicitly tolerated by the US Treasury.

Of course, for Japan and the yen, renminbi devaluation tolerated by the United States would add new fuel to the yen’s decline. So, while the risk of the United States accusing Japan of currency manipulation and engaging in a currency war is low, the possibility that it would tolerate the start of a currency war in Asia may well be underestimated as a next trip wire for dollar strength.

From a Strong Dollar to the Next US Recession

Of course, dollar strength will not be in the United States’ best interest forever. The turning point will come when US recession and deflation risks overpower the current inflationary pressures. More specifically, that point comes when Fed rate hikes begin to cut into US asset prices in general, and US equities in particular.

Never before has the combination of rising rates and falling corporate profits not brought troubles to Wall Street—a bear market at best, a crash at worst. And nothing will focus the minds of the US policy elite like the specter of asset deflation.

The numbers speak for themselves. With just about 40–45 percent of US listed-company earnings coming from global sales, a strong dollar forces weaker earnings. So, while a strong-dollar policy is a welcome tool in the fight against consumer price inflation right now, eventually a switch to a weak-dollar policy will become necessary.

Of course, we can debate whether, in the United States, “this time is different”; whether the threat of stubbornly high consumer price inflation cutting the purchasing power of the people is more important than the loss of capital gains on Wall Street. The Main Street versus Wall Street debate is very real. However, in practical terms for investors, a crash on Wall Street is poised to deliver an about-turn in Fed priorities faster than you can say “American dream.” This is how the dollar’s strong run will end.

US Stagnation Fueling Protectionism in the Run-up to 2024

The bad news is that reality probably won’t be that clear-cut. It is easy to imagine what will happen in the extremes of an inflationary boom and a deflationary bust. What about something more real world, more messy, less clear-cut? Many serious forecasters are predicting a US stagnation scenario—i.e., stubborn but no-longer-accelerating inflation, with growth (and Wall Street) not crashing, rather just meandering and going nowhere.

What are the policy options then?

In my view, the US stagnation scenario will also make it tempting for politicians and policymakers to begin advocating a switch to a weak-dollar policy. The potential windfall to help turn around corporate fortunes is one reason. A more worrying dynamic is that US stagnation is poised to fuel a next wave of protectionism.

Blaming “unfair” cheap imports, pointing to China, Mexico, and Japan, then accusing them of taking jobs from US workers becomes a more tempting narrative the longer stagnation depresses any feel-good factor among US voters. This isn’t likely now, in my view—not for the 2022 mid-term elections (inflation is the more immediate problem this year)—but it becomes a credible scenario for the 2024 presidential fight.

Personally, I worry more about stagnation feeding populism more so than inflation. Under inflation, there are winners and losers. But under stagnation, all you get is an increasingly corrosive disillusionment among every part of society. The American dream very much depends on the celebration of winners; maybe that’s why stagnation will not be tolerated for long. But to get out of it, promises of radical, populist, “only I can fix it” extremist solutions are bound to gain political currency.

Be that as it may, as far as global currency markets are concerned, the higher the US stagnation risk the greater the risk of the United States abandoning its current strong-dollar policy. Moreover, who will want to buy—or even hold—dollars if US interest rates, equities, and real estate prices are going nowhere?

Who Will Buy Japan Assets?

So, it looks like it will become easier to argue for selling US assets as the United States cycle flips from inflationary boom to either frustrating stagnation or deflationary bust. But for the yen to strengthen, investors will have to buy Japan. Why, and when, will this happen? Who will do the buying?

The last point is key, in my view. There is plenty of great analysis demonstrating Japan is cheap. Here are just some of the highlights:

- Japanese equities trade on a 13-times price-to-earnings (PE) multiple, which is cheap against its own 30-year history as well as against the 22-times PE you pay for US equities (TOPIX vs SPX500)

- Japanese labor costs are now down to half (!!) of US ones, $34,000 in Japan versus $69,000 in the United States

- A Big Mac costs ¥399 in Tokyo versus $5.30 in LA, so a US tourist could get two for one

Or at least they could if Japan allowed free travel. Personally, I think the most immediate and impactful way to begin creating new marginal demand for yen is for Kishida to open Japan’s borders. Inbound tourists spent about ¥5 trillion per annum before they were shut out. Although small in absolute terms, relative to the roughly ¥500 trillion daily currency market transactions, creating net new demand for yen is poised to have a positive impact. Markets thrive on new marginal demand.

Welcome to the World, Japan Service Sector Workers and Entrepreneurs

Structurally, the fact that relative Japanese labor costs have fallen so dramatically does open opportunities for more substantial global arbitrage, creating demand for yen. Here, don’t think industrial workers, but rather computer coding, information technology, and other location-agnostic service workers. A yoga class via Zoom with a teacher in Tokyo is now almost half the price of one taught by a Los Angeles- or New York-based yogi.

In fact, several US and Israeli venture capital firms have begun scouting for software engineers based in Tokyo, Fukuoka, or Osaka to do work they had originally planned to have done in Vietnam. Again, Japan engineers are now about 30-percent cheaper than their Vietnamese competitors—never mind Silicon Valley ones.

“Japanese labor costs are now down to half (!!) of US ones, $34,000 in Japan versus $69,000 in the United States.”

Clear speak: The combination of relative cheapness and the realities of remote work and Zoom-based individual services having become more acceptable suggests there is a real chance the world will begin to buy more Japanese services. More specifically, the entrepreneurial opportunities for Japan here are enormous as a much broader section of the service sector transitions from local-only and non-tradeable to global and tradeable. Bonzai classes from a true bonzai master, anyone? This is true not just for traditional Japanese expertise but, more importantly, for newly created Japanese deep tech, patents, and all forms of intellectual property-based innovation. I expect a buying spree by US venture capitalists, snatching up previously hidden innovation bargains created by Japanese private and public scientists and engineers.

Soft Onshoring? Yes. Hard Onshoring? No.

Against this, it is highly unlikely the world will begin to build factories here in Japan. Labor costs are one factor in deciding where to build a factory, but much more important is proximity to market and suppliers. Just look at how difficult it was for the government to persuade Taiwan Semiconductor Manufacturing Company Limited and Sony Semiconductor Solutions Corporation to commit to building a new factory here in Japan.

Labor costs matter in the service sector much more so than in the industrial sector, where capital costs, stakeholder and supplier proximity, and end-market reach are the much more dominant factors. So yes, soft-onshoring—global service sector companies raising their Japan-based footprint—absolutely; but hard-onshoring by industrial companies is unlikely, in my view. Watch for a pickup in inward direct investment, with more service sector global giants buying into Japan, following PayPal Holdings, Inc.’s $2.4 billion acquisition of Tokyo buy now, pay later startup Paidy last September, and the growing success stories of Salesforce, Inc., Amazon Japan G.K., Yahoo Japan Corporation, and law firm Morrison & Foerester LLP here in Japan, to name just a few.

Clear speak: in the coming months, I shall watch carefully for signs of a pick-up in cross-border merger-and-acquisition (M&A) flows into Japan for a possible source of new marginal demand for yen that could help break the current depreciation trend.

Big Guns to the Rescue

When all is said and done, however, Japanese investors hold the key to the fate of the yen. Japan’s status as one of the major global creditors dictates as much. As long as Japanese institutional and retail investors refuse to invest in their own markets and, instead, continue to prefer global or US assets, the case for yen appreciation will be hard to substantiate.

Here it is interesting to recall the history of the world’s single biggest asset manager, Japan’s Government Pension Investment Fund (GPIF). The GPIF manages $1.7 trillion, of which about 26 percent is in global bonds and 24 percent in global stocks. In all the grandstanding about the merits or demerits of yen depreciation, it should not be forgotten that Japanese pensioners are thus a major beneficiary of yen depreciation: a 10-percent decrease in value of the currency should create a two to three-percent upside performance windfall profit (obviously depending on hedge ratios and equity/bond markets performance). I am not a public pension actuary, but some friends who are suggest it is quite possible that, at ¥140–150 to the dollar (and on current asset allocation), Japan’s public pension may actually become overfunded.

“Japanese pensioners are thus a major beneficiary of yen depreciation: a 10-percent decrease in value of the currency should create a two to three-percent upside performance windfall profit.”

Importantly, the GPIF contributed greatly to forcing the last major inflection point in the yen’s fortunes when it announced a major reallocation out of domestic Japanese government bonds into global bonds and equities during the early years of former Prime Minister Shinzo Abe’s administration.

Market participants remember well how the GPIF inflection lent credibility and broader confidence that decades of yen appreciation had come to an end. The GPIF showed the money (with Japan Post Bank and Japan Post Insurance adding welcome firepower).

Performance Pressure: GPIF Public Pension Fund Beats Private Managers

Yes, Kuroda’s BOJ launched an all-out attack on deflation in early 2013, but only when Japan’s (and the world’s) largest asset manager began to act and switched asset allocation did the yen’s fortunes inflect from decades of appreciation towards depreciation. In other words, the GPIF became the primary “agent” for transmitting monetary priorities into the real world.

No, this is not a conspiracy theory. Both the BOJ’s and the GPIF’s assets are owned by the same principal, the Japanese general public. What is interesting, however, is that Japanese private pension managers, whose principals are not the general public but company- or industry-specific employees and pensioners, did not follow the GPIF’s lead and, to this day, have maintained much more conservative allocations to global securities. In contrast to the approximately 50-percent allocation to non-yen assets by the GPIF, private pension managers have slightly less than 30 percent in overseas securities.

Given the now accelerating trend of yen depreciation, the relative outperformance of the public GPIF fund over the private, “independent” ones will, before long, add more pressure for long-overdue professionalization of the stewards of Japanese private-pension schemes. There is no question the GPIF is a best-in-class global steward of capital, while many private pension schemes here are still ensnared in clientelism, cushy amakudari (descent from heaven) positions, and a general lack of financial professionalism.

The $850 Billion Question

When will the GPIF cut non-yen allocations? The bottom line is this: When predicting the yen’s fortunes from here, the real focus for practitioners is not so much whether the US Treasury will agree to let the MOF sell its US-dollar reserves, but whether—or more specifically when—the GPIF will cut down on the global allocations that have served it so well since it started buying dollars in 2013–14, when the yen was ¥80–100 to the dollar.

Make no mistake: the GPIF has evolved into the de facto primary agent for BOJ and MOF monetary policy objectives and stands at the very core of Japan’s capitalism in general, and the transmission from savings into investments in particular. The yen will pivot and start appreciating when the GPIF announces a cut in its global allocation in favor of the deep value offered by yen assets.

When will this happen? My money is on right around the time of the Fed’s third rate hike—i.e., when equity markets have no choice but to admit that the risk-reward of buying stocks makes no sense. To wit, an equity earnings yield of five percent and falling (because earnings are in a downward cycle), and a risk-free rate of three percent and rising, will leave no other choice to the financial professionals at the GPIF and other institutions. Contrast that to an earnings yield of 7.5 percent and a risk-free rate of 0.2 percent in Japan, and you know not just where to hide but where outperformance is likely: here in Japan.

Clear speak: Japan’s deeply engrained reputation as an equity “value trap” will be corrected exactly when Japanese investors begin to recommit to their home-country risk-assets markets. If the GPIF were to lead this charge, fellow global long-term investors are bound to follow—sovereign wealth funds in particular.

But Japanese investors will have to show us the money.

Kuroda’s End Game

How can the negative correlation between the yen and Japanese risk assets in general—and Japan equities in particular—be broken? In my personal view, Kuroda is exactly right to force this realization onto local asset allocators by de facto encouraging a currency overshoot toward ¥150–160 to the dollar. The yen can—and will—be a key force to defeat the deeply entrenched bias against domestic risk assets that Japanese asset allocators have been insisting on for more than 30 years.

If I am right, the current policy decoupling between the BOJ and the Fed will lead to a much more fundamental parting. When Japanese investors begin buying Japanese risk assets instead of non-yen ones, Japanese equities will begin to rise in tandem with yen appreciation.

Although still a long shot at this stage, here is the real escape hatch for Japan from deflation. The long-established negative correlation between Japanese stocks and the currency must be broken. The fact that, for the past 30 years, Japanese equities only go up when the yen goes down while yen appreciation always depresses local stock markets.

“When Japanese investors begin buying Japanese risk assets instead of non-yen ones, Japanese equities will begin to rise in tandem with yen appreciation.”

For this to be supported by fundamentals, domestic Japanese profit margins will have to rise to above those earned from overseas operations and sales.

Here, Kuroda is doing his bit by encouraging yen depreciation, but his efforts will be in vain if Kishida and his stewards of industrial policy do not follow through. For Japanese corporate profits to rise despite yen appreciation, Japan needs a serious round of industrial reorganization and domestic investment.

This is because yen depreciation offers a potentially misleading path. At ¥110 to the dollar, Toyota Motor Corporation’s most profitable factories were the ones in the United States; at ¥130, the ones in Japan will reclaim that spot. However, this windfall is unlikely to last due to the inherent volatility and cyclicality of any exchange rate. As explained above, the moment the Fed changes direction as US recession risks rise, the dollar is set to fall.

From Kuroda’s Cost-Push Stock Therapy …

Sustainable improvements in productivity and profitability will have to be earned through business investment at the level of individual companies and industrial reorganization at the sector and macro levels.

In other words, Kishida and his team must focus on removing regulatory obstacles to industry consolidation, incentivize M&A, and push harder for technological upgrade and capital deepening. Importantly, the current round of cost-push inflation actually creates a strong tailwind for this, because companies with outdated technology and old-fashioned customer acquisition strategies are poised to be squeezed out and lose market share which, in turn, will force them to either start investing in better human and physical capital or have them seriously considering M&A.

To wit, in Japan’s various industries and sectors—from hairdressers to banks to machine tool makers—the top three companies in each command barely 15 percent of their market on average, while in the United States the top three control about 33 percent. This degree of excess competition is also born out when comparing listed companies. US equity markets are almost seven times larger than those in Japan (by market capitalization), but the number of listed companies is almost the same: 4,266 in the United States versus 3,754 in Japan. In other words, Japan Inc. is as good a definition of “red ocean” cut-throat competition as you’ll find.

… to Kishida’s New Capitalism

There is no question that, since the end of the bubble in the early 1990s, Japan’s model of capitalism became increasingly focused on trying to shelter local companies from the forces of asset deflation, technology-induced disruption, rising capital costs, or other forces of “creative destruction” by providing more or less free capital.

Twenty years on, the result is a capitalism marked more by zombie companies that drag down industry and macroeconomic performance, productivity, and financial returns rather than by global top performers. This is where Kishida’s promise of a new capitalism could have real meaning. If new capitalism marks a departure from this zombie capitalism, and actually seeks to incentivize sector-by-sector industrial reorganization and streamlining, then prospects for a sustainable decoupling of Japan’s financial performance from the exchange rate dependency will come into sight. I know this is a big if, but let’s give optimism a chance.

“If new capitalism marks a departure from this zombie capitalism, and actually seeks to incentivize sector-by-sector industrial reorganization and streamlining, then prospects for a sustainable decoupling of Japan’s financial performance from the exchange rate dependency will come into sight.”

Clear speak: if the current pain of cost-push inflation delivers long overdue industrial reorganization and the emergence of true Japanese national champions, the GPIF and other professional investors will be rewarded handsomely—not just from a tactically expedient increase in yen equity allocations because of a Wall Street downcycle, but from a strategic Japan overweight position where yen companies deliver rising returns independent of the currency’s fortunes.

Either way, the yen’s decline will stop and reverse exactly when Japanese investors begin buying their mother markets here in Japan. With a little luck, they’ll do so not just for fear of a US crash, but for realistic expectation that Japanese corporate leaders will not just sweat existing assets but begin to actually invest in both human and physical capital at home.

That’s the optimist’s view. Until then, a pragmatist should prepare for parabolic speculative overshoot towards ¥150–160.

MPower Partners

Japan has incredible potential to support innovative startups and for strong economic growth. Yet it continues to fall short compared with the United States and many other countries. Why is this? What can be done to turn the tide, energize business, and bring greater diversity and opportunity to the country? These questions and more were addressed on July 19, when the American Chamber of Commerce in Japan welcomed Kathy Matsui, Yumiko Murakami, and Miwa Seki, the co-founders of MPower Partners, Japan’s first global venture capital (VC) fund focused on environmental, social, and governance (ESG) criteria.

Japan's first ESG venture capital fund

Japan has incredible potential to support innovative startups and for strong economic growth. Yet it continues to fall short compared with the United States and many other countries. Why is this? What can be done to turn the tide, energize business, and bring greater diversity and opportunity to the country?

These questions and more were addressed on July 19, when the American Chamber of Commerce in Japan welcomed Kathy Matsui, Yumiko Murakami, and Miwa Seki, the co-founders of MPower Partners, Japan’s first global venture capital (VC) fund focused on environmental, social, and governance (ESG) criteria. Managing Director Eriko Suzuki joined the three general partners for the virtual event co-hosted by the Women in Business, Alternative Investment, Sustainability, and Kansai Diversity and Inclusion Committees.

Launched in June, MPower is on a mission to empower startups that are providing tech-enabled solutions to societal challenges and to drive sustainable growth through ESG integration.

During the enlightening panel discussion, moderated by Association of Women in Finance President Yuki Hasegawa, the general partners and managing director covered a wide range of topics, including the challenges facing women founders, the importance of diversity on boards, why Japan is falling short of its potential, and why MPower has chosen to focus on startups rather than larger established companies.

Idiosyncrasies

The session began with Hasegawa asking how Japan differs from other countries when it comes to economic potential and ESG.

Murakami explained that, during her eight years with the Organisation for Economic Co-operation and Development (OECD), where she was head of the OECD Tokyo Centre, she worked with a number of interesting data sets which helped her see common elements in different scenarios that lead to economic growth.

“You need to have people who are well educated, you need to have money to invest, and you need to have very good social infrastructure as well as general stability in the society,” she noted, adding that a high level of technology is key.

“When you look at a lot of the data points around those metrics, Japan does extremely well. It is one of the best countries, which has all the elements necessary [in order] to have very strong economic conditions.

“Yet, Japan has not done all that well—especially over the past 20–30 years—relative to the United States and countries in Europe or even Asia,” she said.

This left Murakami wondering what is missing in Japan.

“You’ve got all of these great things—people, technology, money, a very stable social and political environment—and realizing this was actually one of the triggers where I started to think, what can I do? What can we do to change that?”

Matsui expanded on this.

“At least for me, I felt the sense of urgency. There was so much potential, but the situation, or the conditions, in this country didn’t feel urgent enough,’’ said the former vice-chair and chief Japan equity strategist at Goldman Sachs Japan. She retired from the company at the end of 2020 to start MPower.

“We know that Japan needs innovation. We know that Japan needs to leverage its human capital. We know that there’s ¥2,000 trillion in cash sitting under futons. So, who’s going to make that change? Who’s going to start that progress?” she asked. “We are, perhaps, one small grain of salt in this vast landscape, but what is it that we can bring to this dialogue from our own experiences and, frankly, what do we want to do with the next chapter of our lives? That’s what prompted this whole idea generation.”

Diversity also played a key role in the genesis of MPower, added Seki, an associate professor at Kyorin University who spent more than 20 years at Morgan Stanley and Clay Finlay. This is something that she, Matsui, and Murakami felt was lacking in Japan which they could bring to the table to help address the lack of global perspective that sometimes hampers Japan’s growth.

Personal Stories

While the struggle of women founders to find equal footing with men remains a serious issue in 2021, Murakami shared the inspiring story of her mother’s entrepreneurial spirit and success three decades ago.

A housewife until age 47, she opened her first “tiny little drugstore” as she neared 50. The shop did very well, so she opened another, and another. Soon she was running the largest drugstore chain in western Japan.

“She was the only woman in this business, and no one else was like her, which really helped her in terms of understanding the marketplace and where opportunities were,” Murakami explained. “This is going back to the 1990s. Japan was starting to have this demographic crisis, but no one knew about it—except for housewives, who were taking care of their in-laws. In my hometown, [aging] was already starting to occur, but it was really not visible to anyone else—especially not to those big companies based in Tokyo. So she was able to identify this incredible opportunity basically to cater to the silver economy.”

Today, the silver economy—products and services designed to meet the needs of people aged 60 and over—is very lucrative, but at the time that Murakami’s mother was building her drugstore business no one yet knew this was going to be the case. It was a different perspective that allowed her to see things from outside. “My mother, because she was a minority in this business, was able to identify that,” Murakami said.

The story also highlights something that remains an obstacle 30 years later, something MPower hopes to change.

“It was really hard for her to obtain capital. Because she was a woman, because she was a housewife, she had to use my father’s name to take out loans. It was the only way for her to raise funds for her business expansion,” Murakami continued. “So, the moral of the story is, I think, opportunities like that are actually abundant. You just have to be able to look at the same opportunity or situation from a different angle and realize, oh, that is not yet addressed in terms of potential demand or needs. And I think that’s really exciting for us, because there are so many opportunities that have not been discovered. I think we can unlock some of these really interesting opportunities in the Japanese business setting.”

Focus on ESG

Moving to the foundation of MPower, Hasegawa asked about the areas on which the group would like to focus.

Suzuki, a former general partner of global VC fund Fresco Capital and former director of Mistletoe, a social impact-focused VC fund founded by Taizo Son, noted that while most people are familiar with the concept of ESG, they may not realize that it is still early days for ESG in the VC space. MPower sees this as an opportunity and is working on solutions to help startups.

“What we mean by early is there aren’t many frameworks or agreed-upon metrics to measure ESG progress within the startups and private-company space,” she explained. “We are assembling a lot of tools on our end and customizing them for each company. It differs by industry, so startups in a healthcare sector would have different metrics from a startup in a pure software and digital transformation sector. It is customized by the industry of the startup, and also slightly by stage.”

Given that startups in the early stage of development will have a different environment and probably fewer resources compared with those in later stages, MPower is focusing on mid- to late-stage companies, Suzuki said. This is because, she explained, they have a more established foundation on which to incorporate ESG principles.

Globally, ESG is becoming more important to venture capitalists, according to Suzuki. This is especially true in Europe. In the United States, while ESG is important, there has been more focus on diversity, equity, and inclusion given the social dialogue around gender and racial diversity that has been taking place there in recent years. When it comes to ESG, which parts of the acronym are most important differs by company, and some organizations may choose to focus on just one.

“Our stance, and I think this is the overall trend, is that they are all important,” Suzuki said. “But what we are seeing is that startups may not realize this. They might think, oh, we are doing something in [a particular] sector—perhaps it’s an edtech company focusing on social, the S—and we’re contributing to progress in society, so we are okay. However, investors are looking at all aspects and, once these companies go public, they will be looked up on the E and the G as well. So, we are tailoring a lot of these materiality concepts.”

Case Study

Suzuki gave as an example of MPower’s approach its investment in Japanese startup UniFa Inc., which uses the latest technologies to support safe and secure childcare environments by reducing the workload on childcare workers. The company is in the mid to late stages of its launch.

“They are growing and are on their way to becoming a public company quite soon. We have invested in them because we think they are a growing business with all the types of innovation needed in Japan. This is a childtech company that, in Japan, is selling into childcare centers—public and private—and they start out by selling sensors to prevent sudden infant death syndrome. These are high-margin, high-technology solutions. With that, they build relationships with these childcare centers and provide other forms of digital transformation tools for the back end, to enable the service providers to focus on actually taking care of the children rather than doing a lot of paperwork.”

Suzuki explained that, before MPower invests in a company, they want to make certain that the founders are interested in making ESG part of their core business. “We truly believe that incorporating ESG will grow the business and contribute to the bottom line and enterprise value.” They identified such a desire in the leaders of UniFa prior to investment, and the company is very willing to work with stakeholders on all aspects of ESG.

“In terms of next steps, we will be identifying together with the company—and the company itself will be setting—the most relevant ESG metrics that they want to follow, and we will be working with them very periodically, at least quarterly, to achieve some of these,” she said. “We understand the challenges, because startups are resource constrained but, at the same time, they need to grow two or threefold per year. So, they need to balance what types of initiatives they can take on. But we really tried to align with the company that this is not a cost but is really an investment in their growth.”

Why VC?

Given that Murakami, Seki, and Matsui have a collective background that is much more in the public equity market rather than VC, they are often asked why MPower is focusing on unlisted companies as a VC fund rather than as a public market investor. Matsui explained that it is a matter of finding the right companies with which there is a better chance of achieving ESG goals.

Noting fast-moving global trends toward more diversity on boards, she gave as an example Nasdaq, which has a woman president. A change to the requirements being proposed would mandate that a company have at least two diverse board directors to be listed on the exchange.

And such moves are not limited to the United States.

“We’ve already seen here in Japan, over the past few years, institutional investors—be it State Street Global or Goldman Sachs [in] asset management, or proxy advisors like Glass Lewis—demanding in their voting guidelines that at least one diverse board member be present—or at least be worked on—otherwise, they will cast an automatic no vote against management,” Matsui said.

She also noted that many Japanese startups with which MPower speaks say that they have a strong desire to diversify their boards and are desperately looking for candidates. So, if you are interested in becoming a board member, MPower would like to know, as they are starting to help match companies and candidates. “It’s quite different, of course, serving on the board of a startup versus that of a large publicly traded company, but we think there are a lot of amazing learning opportunities that could be had,” Matsui added.

Returning to the reason MPower is focusing on startups, she explained: “We felt that trying to change larger, established companies is quite difficult for a whole host of obvious reasons. It’s important here to recognize that we know there’s a lot of what we call greenwash risk. It’s very easy to tick boxes but much more difficult to actually implement ESG in your core business strategies.”

For MPower to achieve its goals, the founders feel that it is better to work with startups and younger companies, “maybe in their teenage phase,” as Matsui put it, to integrate ESG.

“Perhaps it’s not easy, of course, but it’s easier to integrate ESG values and principles at that younger stage of a company’s development, before they go public, before they are acquired,” she explained. “And we’ve been very positively surprised. We look at domestic Japanese startups as well as overseas startups. Maybe its selection bias, but most of the entrepreneurs we’re meeting are very keen to fix the ESG areas that they deem weak. So, we’re really positively surprised by the direction thus far.”

Fostering Change

Matsui recalled with a laugh something said to her by a foreign investor when she began researching Japanese corporate governance more than 20 years ago: “Kathy, you’re trying to convince vegetarians to become carnivores.” But eventually Japan adopted a stewardship code, in 2014, and a corporate governance code, in 2015. Despite these requirements, the management of many companies is seen as reluctantly going along with something they know they must do but which they “do not really have in the bottom of their hearts and do not really get,” Matsui said. Many do not want to spend money on initiatives around gender diversity, for example. They don’t see the benefit.

“I think the biggest roadblock is that of mindset, [understanding] that this is not a cost, but an investment in their future,” she continued. “And I think that a lot of the governance-related challenges that Japanese companies—at least the large ones—have faced, if you look at the root cause of these problems, stem from an echo-chamber decision-making process. Their past presidents or chairmen—even though they don’t have an official vote—are all hanging around. We call it ghosts in the boardroom.”

Once a company does see the need and benefit, the next step is helping them understand that the process is a marathon, not a sprint, Matsui explained. It must be understood that all the training and education involved in the transition is being done because it makes business and economic sense, not because it is being mandated by regulations.

“If you don’t start with that argument, I think it’s very, very difficult to convince the naysayers or the skeptics why this is important,” she said. “So, to me, having a different perspective and a different point of view to challenge the status quo is one of the most important things that diversity of thought brings to the discussion.”

Social Solutions

What is it that attracts MPower to the ESG space, and what do the partners see as Japan’s competitive advantages and weaknesses?

Seki began her answer by highlighting Japan’s position as a kadai senshin koku, a country with many emerging social issues to tackle. Aging is at the forefront, but the lack of diversity in corporate management and low productivity are problems as well.

“Identifying startups to provide the best solutions to those social issues will be a huge opportunity for us,” she said. “Putting ESG aside, there is a huge funding gap in the VC field, especially in the growth to later-stage funding. That provides us with a huge opportunity to support those startups that are willing to—or are trying to—go global. And the lack of diversity and the aging of society are also great opportunities for companies—and for us as well—to bring diversity to the table.”

Matsui noted that Japanese companies tend to score relatively high for the E in global sustainability studies, but are weaker when it comes to the S and the G. And in terms of the E, meeting the government’s ambitious target of being carbon neutral by 2050 will bring serious challenges to corporations in Japan.

“What some companies are complaining about is that this effectively is a tax on them, if they have to go in that direction,” Matsui said. “So, even though on the surface Japanese companies look like they’re really stronger in the E, just given how rapidly the world is changing they are going to have to double down on their efforts on the E. But also on the S and the G there is a lot of work to be to be done. That is an absolute opportunity for a fund like ours and investors like ourselves to help companies who want to provide those solutions in those spaces.”

Frameworks and Urgency

One need only turn on the news to see how climate change is impacting our lives on a daily basis. Murakami said there has been a lot of discussion about climate risk, but people are beginning to realize that the problem isn’t going away. Efforts must be accelerated, and more agreement on how to measure and report the effectiveness of actions is needed.

Among the initiatives underway this year are the United Nations Climate Change Conference (COP26), to be held November 1–12 in Glasgow, Scotland, and a working group announced on March 22 by the International Financial Reporting Standards (IFRS) Foundation, “to accelerate convergence in global sustainability reporting standards focused on enterprise value, and to undertake technical preparation for a potential international sustainability reporting standards board under the governance of the IFRS Foundation.”

Murakami said these are very exciting moves that everyone should be watching, because one of the problems is that, with so many frameworks in use around the world, it is difficult to really measure what is driving the climate change we are seeing. “Yes, it is hotter, it rains more, and we feel climate change impacting us … but it’s difficult to move the needle when you don’t know where the needle stands.”

MPower has been developing its own framework for measuring and reporting, one better suited to VCs than to large companies, and they have looked at various existing frameworks in the process. But Murakami is looking forward to a consolidation of the hundreds that are currently out there down to just two or three globally accepted standards that can be used as guidelines for companies to measure where they stand on ESG. “I think that’s a very exciting development that we’re actually watching this year.”

Shifting Needs

The aging of society, expanding role of technology, and efforts to mitigate the impact of climate change are all remaking the job-market landscape. Hasegawa asked if the Japanese government is doing enough to address the need for skills in emerging areas and the potential displacement of workers as industries change as a result of the country’s pursuit of carbon neutrality.

Murakami said one of the greatest challenges for Japan is to address the very rigid employment system that makes it difficult for people to reskill themselves and find jobs.

“One thing the government really needs to do is to encourage companies to become a lot more flexible and understand the changing demands of the labor market—and of their customers as well—so that they can adjust the skill sets of their employees by not only reskilling or upskilling them, but also making sure that they can provide opportunities for people who may be joining a company at the age of 25 or 35 instead of 22,” she said.

In addition, there must also be a merit-based compensation system and promotion scheme. That is an area where Murakami feels many companies are trying to change, but have not fully done so yet—in part due to policies and regulations that are preventing them from moving to more merit-based systems.

Empowering Women

While MPower is not focused exclusively on female founders, encouraging more women to pursue entrepreneurial paths and working to close the gender gap in financing is one of their goals. And as Murakami’s story about her mother shows, women often bring a perspective and insight that reveals a solution which men may not see.

But traveling the road to that solution requires money, and one challenge for women looking to raise capital is that most investors are male. Suzuki pointed out that fewer than 10 percent of decision-making investors in the VC space are female, and just four to five percent of VC is invested in woman founders.

A common belief among investors, Suzuki said, is that women are unable to take risks. But studies have found that female founders actually return capital at a greater rate than their male counterparts. They may also be more conservative in terms of the projections they share with investors compared with their male peers, who tend to be more aggressive. But whereas the men don’t necessarily hit their targets, the women tend to be very stable.

“So, there’s a lot of great potential there, and we’d love to see entrepreneurialism in various areas solving some of the issues that women are facing,” Suzuki added, pointing out how the caretaking burden disproportionately falls on women. “That is something we hope to see in the next generation.”

Attracting Global Investment

Two recent papers produced by committees of the ACCJ have highlighted the considerable opportunities that would result from changes to regulations that currently hinder Japan’s financial sector from attaining its full potential. And with the Japanese government committed to raising Tokyo’s profile as one of the world’s top financial centers, the committees are hopeful that regulatory authorities here might embrace some of the proposals.

Ideas for making Japan a top financial center

Listen to this story:

Two recent papers produced by committees of the American Chamber of Commerce in Japan (ACCJ) have highlighted the considerable opportunities that would result from changes to regulations that currently hinder Japan’s financial sector from attaining its full potential. And with the Japanese government committed to raising Tokyo’s profile as one of the world’s top financial centers, the committees are hopeful that regulatory authorities here might embrace some of the proposals.

The Investment Management Committee published a viewpoint entitled Relax or Eliminate Unrelated and Onerous Regulatory Requirements for Marketing of Offshore Funds to Professional Investors Conducted by Global Investment Managers, while the Financial Services Forum released a white paper headlined Reimagining Japan as a Global Financial Center, the latter proposing changes that would drive the nation’s long-term economic growth.

License to Sell

Japan’s financial regulations are designed to protect investors, both retail and institutional, which is a “worthwhile goal” according to David Nichols, executive advisor at EY Strategy and Consulting Co., Ltd. The type of investment is determined by the definition of the investment and the sales license held by the distributor.

“The licenses entail certain responsibilities—some fiduciary and some customer best-interest,” said Nichols, who also chairs the Investment Management Committee.

“While distributors do not have a fiduciary duty to their clients, they are holding their customers’ security purchases in firm accounts,” he added. “As such, the state of the distributors’ balance sheets can impact the client holdings. If the distributor goes bankrupt, clients may have difficulty accessing their investments.” As a result, the Type 1 license required by a distributor has capital adequacy requirements to safeguard investors.

While offshore funds fall under the definition of securities that can only be sold by distributors with a Type 1 license, the fund assets are not part of a distributor’s balance sheet and, therefore, are not impacted by the health of that balance sheet, Nichols pointed out.

“So, the reason the regulations are in force is that offshore funds have been classified as a security but do not hold the same dependency on the distributor’s balance sheet as a normal security does, since the fund assets are held by an independent custodian,” he explained, describing the situation as “an unintended consequence of regulations intended to protect investors.”

To correct the situation would require a root-and-branch revision of the 2006 Financial Instruments and Exchange Act, which would be a major undertaking and would require an amendment approved by the national Diet. Instead, the ACCJ is proposing some administrative changes that the Financial Services Agency can enact and “that would get us to materially the same place,” Nichols said.

Norihiko Tsukada, managing director and head of compliance at BlackRock Japan Co., Ltd. and vice-chair of the Investment Management Committee, identified “certain off-site monitoring items, including daily calculations of capital ratios” as one regulation that is unnecessarily obstructive, although he points out that regulations in Japan are broadly equivalent to those of other jurisdictions. In the United States, however, limitations are less of a concern, as the market there is sufficiently large to make it economically feasible to package investments in US onshore vehicles.

Lost in Translation

Distributors in Japan also face administrative hurdles and language requirements that make it more complicated to set up and run an asset management business. That should be a concern since Tokyo has designs on a larger role in the global financial services market.

The committee has recommended that regulations surrounding the offsite monitoring of investment management companies (IMCs) should be relaxed, as certain reporting items are not relevant to the activities of global IMCs, along with the initial registration process for distributors of standard Type 1 Financial Instruments Business (FIB).

“Tailoring regulatory requirements to address relevant business risks will not impact client protection,” the paper emphasizes, adding that “such relaxation of regulatory requirements would improve the appeal of Japan to foreign investment managers interested in establishing a presence in Japan, and would be consistent with the [government of Japan’s] objectives to promote Tokyo as a global financial city.”

The solution, the committee suggests, would be the creation of a new type of FIB, that might be called a “solicitation-only” Type 1 FIB.

Seize the Moment